Image 1 of 4

Image 1 of 4

Image 2 of 4

Image 2 of 4

Image 3 of 4

Image 3 of 4

Image 4 of 4

Image 4 of 4

Every major decision a public company makes — issuing debt, buying back shares, paying dividends, acquiring another company — is a capital allocation decision. These decisions determine whether shareholder value is created or destroyed, often more decisively than operational performance.

This guide teaches you how corporations manage their financial resources and how to read corporate financial decisions as signals about management quality, company health, and future returns.

WHAT'S INSIDE — 8 CHAPTERS:

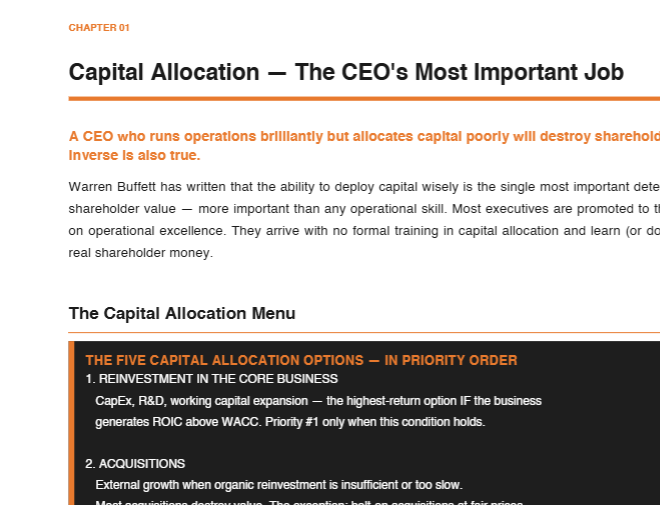

→ Capital Allocation — The CEO's Most Important Job

Warren Buffett's view: the ability to deploy capital wisely is the single most important determinant of long-run shareholder value. The five capital allocation options in priority order — core business reinvestment, acquisitions, debt repayment, dividends, and share buybacks — and the ROIC vs. WACC framework that determines which option is correct in any given situation. The historical record of the great capital allocators: Henry Singleton, John Malone, Tom Murphy, and what they did differently.

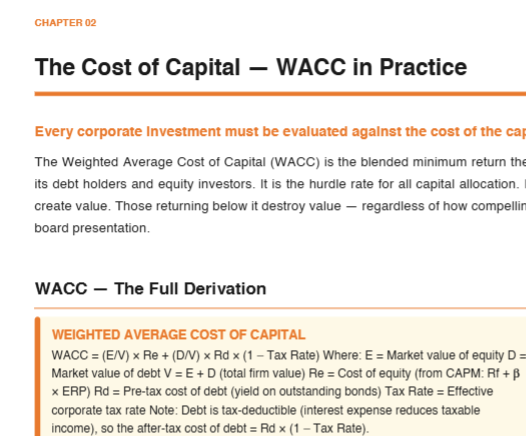

→ The Cost of Capital — WACC in Practice

The full WACC derivation with every input explained — equity weight, cost of equity via CAPM (risk-free rate, equity risk premium, beta), debt weight, pre-tax cost of debt, tax shield. A complete CAPM input table with current ranges and sources. WACC ranges by industry from regulated utilities (5–7%) through early-stage growth tech (15–25%).

→ Debt Issuance — When, Why, and How Much

Eight corporate debt types — investment grade bonds, high yield, leveraged loans, revolving credit facilities, TLA, TLB, convertible notes, and mezzanine — with characteristics, typical users, and the key terms to analyze for each. The cost-benefit framework for any leverage decision: tax shield and return amplification as benefits; financial distress costs and reduced strategic flexibility as costs.

→ Equity Issuance and Share Buybacks

The cardinal rule: issue equity when the stock is overvalued. Repurchase when it is undervalued. A five-row value creation and destruction matrix showing the shareholder impact of repurchasing at 60%, 80%, 100%, 120%, and 150%+ of intrinsic value. Apple's $600 billion in buybacks from 2012–2023 as a case study in per-share compounding.

→ Dividends — The Capital Return Signal

A dividend is management's admission that it has more cash than it can deploy above cost of capital. Five dividend policy types — stable/growing, variable, special, none, and hybrid — with the market signal each sends and the appropriate business context for each. The five key dividend metrics with formula, healthy range, and warning signal for each: yield, EPS payout ratio, FCF payout ratio, coverage ratio, and five-year growth CAGR.

→ Mergers & Acquisitions — Value Creation or Destruction?

The academic literature is unambiguous: the average acquisition destroys acquirer shareholder value. Acquirers pay 30–40% average premiums. Most synergies are overestimated. Integration costs are underestimated. CEO incentives favor size over per-share value. This chapter covers the five specific reasons most acquisitions fail — and the four specific circumstances where they actually create value.

→ Capital Structure Theory

The two foundational academic frameworks: Modigliani-Miller (capital structure irrelevant in perfect markets) and its real-world refutation through the trade-off theory (tax benefits of debt vs. financial distress costs) and the pecking order theory (internal funds first, debt second, equity as last resort). Why each framework explains something true and neither explains everything.

→ How Markets React to Corporate Financial Decisions

A ten-row signaling reference: dividend initiation, dividend increase, dividend cut, share buyback announcement, secondary equity offering, large acquisition announcement, debt rating upgrade, debt rating downgrade, unplanned CFO departure, and insider personal share purchases — with the market signal interpretation, typical price reaction, and when to be skeptical for each. The corporate decision that has the highest signal strength: a CEO buying shares with their own money.

WHO THIS IS FOR:

Investors who want to read corporate decisions as signals rather than noise. Finance professionals who want a clean conceptual framework. Anyone studying for CFA, MBA, or investment banking interviews who needs the concepts applied rather than merely defined.

FORMAT: PDF — Instant download. No subscription. Yours forever.

Every major decision a public company makes — issuing debt, buying back shares, paying dividends, acquiring another company — is a capital allocation decision. These decisions determine whether shareholder value is created or destroyed, often more decisively than operational performance.

This guide teaches you how corporations manage their financial resources and how to read corporate financial decisions as signals about management quality, company health, and future returns.

WHAT'S INSIDE — 8 CHAPTERS:

→ Capital Allocation — The CEO's Most Important Job

Warren Buffett's view: the ability to deploy capital wisely is the single most important determinant of long-run shareholder value. The five capital allocation options in priority order — core business reinvestment, acquisitions, debt repayment, dividends, and share buybacks — and the ROIC vs. WACC framework that determines which option is correct in any given situation. The historical record of the great capital allocators: Henry Singleton, John Malone, Tom Murphy, and what they did differently.

→ The Cost of Capital — WACC in Practice

The full WACC derivation with every input explained — equity weight, cost of equity via CAPM (risk-free rate, equity risk premium, beta), debt weight, pre-tax cost of debt, tax shield. A complete CAPM input table with current ranges and sources. WACC ranges by industry from regulated utilities (5–7%) through early-stage growth tech (15–25%).

→ Debt Issuance — When, Why, and How Much

Eight corporate debt types — investment grade bonds, high yield, leveraged loans, revolving credit facilities, TLA, TLB, convertible notes, and mezzanine — with characteristics, typical users, and the key terms to analyze for each. The cost-benefit framework for any leverage decision: tax shield and return amplification as benefits; financial distress costs and reduced strategic flexibility as costs.

→ Equity Issuance and Share Buybacks

The cardinal rule: issue equity when the stock is overvalued. Repurchase when it is undervalued. A five-row value creation and destruction matrix showing the shareholder impact of repurchasing at 60%, 80%, 100%, 120%, and 150%+ of intrinsic value. Apple's $600 billion in buybacks from 2012–2023 as a case study in per-share compounding.

→ Dividends — The Capital Return Signal

A dividend is management's admission that it has more cash than it can deploy above cost of capital. Five dividend policy types — stable/growing, variable, special, none, and hybrid — with the market signal each sends and the appropriate business context for each. The five key dividend metrics with formula, healthy range, and warning signal for each: yield, EPS payout ratio, FCF payout ratio, coverage ratio, and five-year growth CAGR.

→ Mergers & Acquisitions — Value Creation or Destruction?

The academic literature is unambiguous: the average acquisition destroys acquirer shareholder value. Acquirers pay 30–40% average premiums. Most synergies are overestimated. Integration costs are underestimated. CEO incentives favor size over per-share value. This chapter covers the five specific reasons most acquisitions fail — and the four specific circumstances where they actually create value.

→ Capital Structure Theory

The two foundational academic frameworks: Modigliani-Miller (capital structure irrelevant in perfect markets) and its real-world refutation through the trade-off theory (tax benefits of debt vs. financial distress costs) and the pecking order theory (internal funds first, debt second, equity as last resort). Why each framework explains something true and neither explains everything.

→ How Markets React to Corporate Financial Decisions

A ten-row signaling reference: dividend initiation, dividend increase, dividend cut, share buyback announcement, secondary equity offering, large acquisition announcement, debt rating upgrade, debt rating downgrade, unplanned CFO departure, and insider personal share purchases — with the market signal interpretation, typical price reaction, and when to be skeptical for each. The corporate decision that has the highest signal strength: a CEO buying shares with their own money.

WHO THIS IS FOR:

Investors who want to read corporate decisions as signals rather than noise. Finance professionals who want a clean conceptual framework. Anyone studying for CFA, MBA, or investment banking interviews who needs the concepts applied rather than merely defined.

FORMAT: PDF — Instant download. No subscription. Yours forever.