Image 1 of 4

Image 1 of 4

Image 2 of 4

Image 2 of 4

Image 3 of 4

Image 3 of 4

Image 4 of 4

Image 4 of 4

Most personal finance content tells you what to do and then relies on your willpower to execute it. This guide is built differently. It is a systems document — a set of structures, automations, and frameworks that remove willpower from the equation as much as possible, because the research on willpower is unambiguous: it is finite, unreliable, and the worst foundation for financial behavior.

Build the right system. The outcomes follow.

WHAT'S INSIDE — 8 CHAPTERS:

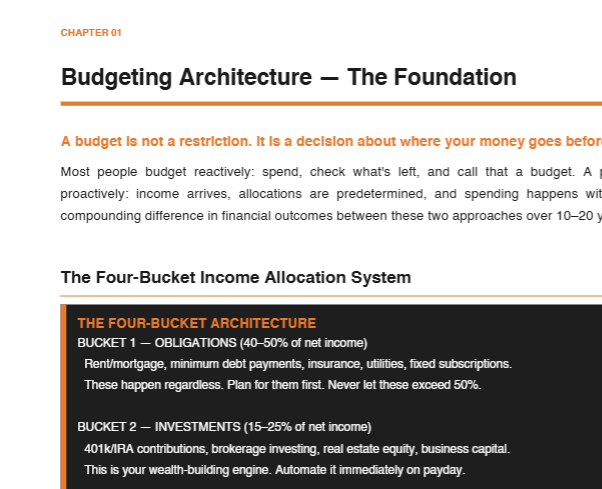

→ Budgeting Architecture — The Foundation

The four-bucket allocation architecture: Obligations (40–50%), Investments (15–25%), Savings (5–15%), and Lifestyle (the remainder). A full target allocation table for nine expense categories with minimum, standard, and wealth-building percentage ranges for each. The zero-based budget method — allocating every dollar to a named purpose until the unallocated remainder reaches exactly zero.

→ Cash Reserve Systems — Layers of Liquidity

A three-layer cash reserve architecture with different purposes, different account structures, and different access rules for each. Layer 1 is the buffer. Layer 2 is the sinking fund system — dedicated monthly savings for planned future expenses (car maintenance, medical, vacation, gifts) that eliminates most 'unexpected' expenses before they arrive. Layer 3 is the true emergency fund. Emergency fund sizing by situation — dual income stable employment through entrepreneur through pre-retirement — with the specific reasoning for each.

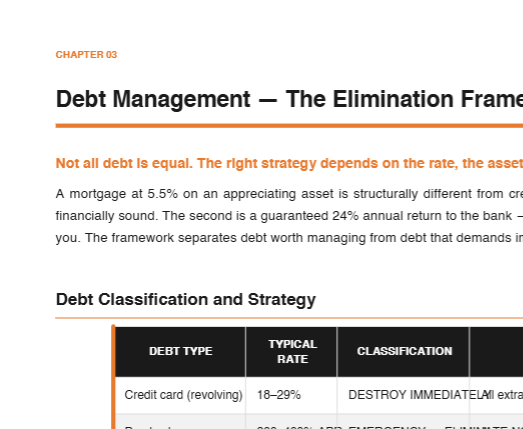

→ Debt Management — The Elimination Framework

A ten-row debt classification table from credit card debt (destroy immediately) through investment property mortgage (maintain as asset financing), with the correct strategy for each. The avalanche vs. snowball comparison with what each optimizes for, who each is best for, and when the hybrid approach makes sense.

→ Savings Automation — Remove the Decision

The most powerful savings strategy is removing the moment of decision. This chapter explains the automation architecture — the exact sequence of transfers on payday — and provides the eight-item automation table with timing, destination, and priority for each. When savings happen automatically before discretionary spending is possible, the behavioral math changes entirely.

→ Investment Allocation — Where the Money Works

The complete investment account hierarchy: 401k match (first dollar, always), HSA (triple tax advantage — the most underused vehicle in personal finance), Roth IRA, Traditional IRA, 401k beyond match, taxable brokerage, and 529. For each: tax treatment, 2024 annual limit, and ideal use case. Plus the four core allocation principles — time horizon dominance, fee compounding math, asset location optimization, and rebalancing discipline.

→ Tax Awareness — The Silent Return Drain

Eight tax optimization strategies with their mechanism, annual impact range, and effort level — from maximizing pre-tax 401k through tax-loss harvesting through the backdoor Roth IRA through asset location. Taxes are the largest single expense for most high-earning individuals. They are also the most negotiable.

→ Insurance & Emergency Planning

The wealth protection checklist most people skip entirely. Seven insurance types — term life, own-occupation disability, health, auto liability, homeowner/renter, umbrella, and long-term care — with what each protects, annual cost, and the most common mistakes for each. Six emergency planning items with specific documentation and action requirements.

→ Net Worth Tracking — The Scoreboard

The precise definition of what to include (and not include) in net worth. Net worth benchmarks by age from the mid-20s through late 50s across four quartiles. The Millionaire Next Door benchmark formula. And the monthly review protocol that converts tracking from an exercise into a behavioral driver.

WHO THIS IS FOR:

Anyone earning a decent income who feels like they have nothing to show for it. People who have tried budgets before and abandoned them. Those who want a financial system that runs on structure rather than discipline.

FORMAT: PDF — Instant download. No subscription. Yours forever.

Most personal finance content tells you what to do and then relies on your willpower to execute it. This guide is built differently. It is a systems document — a set of structures, automations, and frameworks that remove willpower from the equation as much as possible, because the research on willpower is unambiguous: it is finite, unreliable, and the worst foundation for financial behavior.

Build the right system. The outcomes follow.

WHAT'S INSIDE — 8 CHAPTERS:

→ Budgeting Architecture — The Foundation

The four-bucket allocation architecture: Obligations (40–50%), Investments (15–25%), Savings (5–15%), and Lifestyle (the remainder). A full target allocation table for nine expense categories with minimum, standard, and wealth-building percentage ranges for each. The zero-based budget method — allocating every dollar to a named purpose until the unallocated remainder reaches exactly zero.

→ Cash Reserve Systems — Layers of Liquidity

A three-layer cash reserve architecture with different purposes, different account structures, and different access rules for each. Layer 1 is the buffer. Layer 2 is the sinking fund system — dedicated monthly savings for planned future expenses (car maintenance, medical, vacation, gifts) that eliminates most 'unexpected' expenses before they arrive. Layer 3 is the true emergency fund. Emergency fund sizing by situation — dual income stable employment through entrepreneur through pre-retirement — with the specific reasoning for each.

→ Debt Management — The Elimination Framework

A ten-row debt classification table from credit card debt (destroy immediately) through investment property mortgage (maintain as asset financing), with the correct strategy for each. The avalanche vs. snowball comparison with what each optimizes for, who each is best for, and when the hybrid approach makes sense.

→ Savings Automation — Remove the Decision

The most powerful savings strategy is removing the moment of decision. This chapter explains the automation architecture — the exact sequence of transfers on payday — and provides the eight-item automation table with timing, destination, and priority for each. When savings happen automatically before discretionary spending is possible, the behavioral math changes entirely.

→ Investment Allocation — Where the Money Works

The complete investment account hierarchy: 401k match (first dollar, always), HSA (triple tax advantage — the most underused vehicle in personal finance), Roth IRA, Traditional IRA, 401k beyond match, taxable brokerage, and 529. For each: tax treatment, 2024 annual limit, and ideal use case. Plus the four core allocation principles — time horizon dominance, fee compounding math, asset location optimization, and rebalancing discipline.

→ Tax Awareness — The Silent Return Drain

Eight tax optimization strategies with their mechanism, annual impact range, and effort level — from maximizing pre-tax 401k through tax-loss harvesting through the backdoor Roth IRA through asset location. Taxes are the largest single expense for most high-earning individuals. They are also the most negotiable.

→ Insurance & Emergency Planning

The wealth protection checklist most people skip entirely. Seven insurance types — term life, own-occupation disability, health, auto liability, homeowner/renter, umbrella, and long-term care — with what each protects, annual cost, and the most common mistakes for each. Six emergency planning items with specific documentation and action requirements.

→ Net Worth Tracking — The Scoreboard

The precise definition of what to include (and not include) in net worth. Net worth benchmarks by age from the mid-20s through late 50s across four quartiles. The Millionaire Next Door benchmark formula. And the monthly review protocol that converts tracking from an exercise into a behavioral driver.

WHO THIS IS FOR:

Anyone earning a decent income who feels like they have nothing to show for it. People who have tried budgets before and abandoned them. Those who want a financial system that runs on structure rather than discipline.

FORMAT: PDF — Instant download. No subscription. Yours forever.